ZIBS视界丨助理教授邵辉在运筹学权威期刊发表论文

2023.12.29

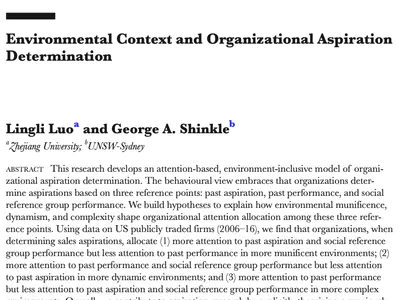

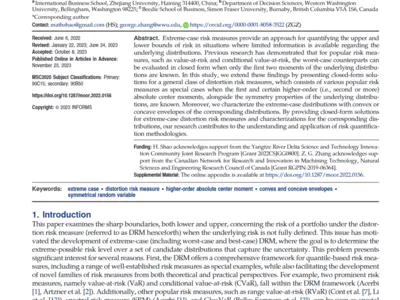

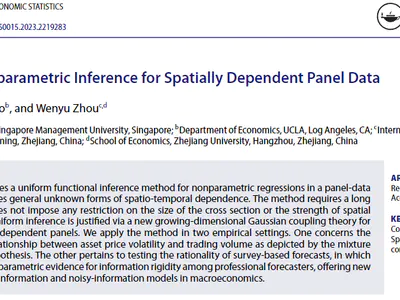

2023年11月,ZIBS助理教授邵辉在运筹学权威期刊Mathematics of Operations Research发表题为“Extreme-Case Distortion Risk Measures: A Unification and Generalization of Closed-Form Solutions”的论文。根据Web of Science数据显示,这是浙江大学学者首次在该期刊上发表论文。

该研究成果阐明了在已知概率分布的一阶和某些高阶绝对中心矩以及概率分布的对称性等形状信息的情况下,可以通过显式解评估极值情况下的DRM和相应的极值情况下的分布,且极端情况下的分布可以用相应扭曲函数的凸包络或凹包络来表征。从理论研究角度来看,该研究结果一般化了大量现有研究结果,如包含了只知道前两个矩时的最坏情况风险价值和最坏情况CVaR。从实用角度来看,极端情况下DRM的显式解为其分布式稳健优化理论提供了极大的可操作性。(点击文末“阅读原文”了解更多)

Mathematics of Operations Research

Mathematics of Operations Research 是美国运筹学与管理科学学会(INFORMS)旗下的重要学术期刊,和Management Science,Operations Research并称运筹学三大权威期刊。该期刊关注在连续、离散和随机优化、数学规划、动态规划、随机过程、随机模型、仿真方法、控制与适应、网络、博弈论和决策理论等领域的数学和计算基础。据该期刊官网介绍,相较于Management Science和Operations Research,发表于Mathematics of Operations Research的论文必须为在数学等理论模型和算法方面取得重大突破,且具备充分数学深度的研究。

摘要

Extreme-case risk measures provide an approach for quantifying the upper and lower bounds of risk in situations where limited information is available regarding the underlying distributions. Previous research has demonstrated that for popular risk measures, such as value-at-risk and conditional value-at-risk, the worst-case counterparts can be evaluated in closed form when only the first two moments of the underlying distributions are known. In this study, we extend these findings by presenting closed-form solutions for a general class of distortion risk measures, which consists of various popular risk measures as special cases when the first and certain higher-order (i.e., second or more) absolute center moments, alongside the symmetry properties of the underlying distributions, are known. Moreover, we characterize the extreme-case distributions with convex or concave envelopes of the corresponding distributions. By providing closed-form solutions for extreme-case distortion risk measures and characterizations for the corresponding distributions, our research contributes to the understanding and application of risk quantification methodologies.

作者简介

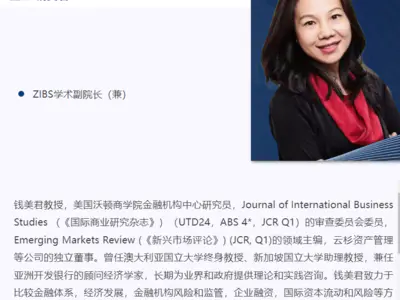

邵辉

ZIBS助理教授

邵辉,北京大学数学博士学位,曾任新加坡国立大学量化金融研究中心和风险管理研究所助理研究员、研究员。研究领域为应用概率论和金融工程,在《Mathematics of Operations Research》、《SIAM Journal on Financial Mathematics》、《Operations Research》、《European Journal of Operational Research》等权威期刊上发表论文。

2024.07.04

2024.07.03

2024.06.30

2024.06.26

2024.06.25

2024.06.17

2024.06.15

2024.06.12

2024.06.11

2024.06.08

2024.06.06

2024.06.05

2024.06.04

2024.06.01

2024.05.31

2024.05.30

2024.05.29

2024.05.29

2024.05.27

2024.05.23

2024.05.22

2024.05.21

2024.05.15

2024.05.13

2024.05.13

2024.05.13

2024.05.11

2024.05.10

2024.05.09

2024.05.07

2024.05.07

2024.05.06

2024.05.06

2024.05.02

2024.05.02

2024.05.01

2024.05.01

2024.04.30

2024.04.29

2024.04.27

2024.04.25

2024.04.24

2024.04.23

2024.04.22

2024.04.18

2024.04.17

2024.04.15

2024.04.14

2024.04.11

2024.04.08

2024.04.08

2024.04.07

2024.04.04

2024.04.03

2024.04.02

2024.04.01

2024.03.30

2024.03.28

2024.03.26

2024.03.24

2024.03.23

2024.03.21

2024.03.15

2024.03.08

2024.03.05

2024.03.01

2024.02.27

2024.02.23

2024.02.21

2024.02.19

2024.02.15

2024.02.13

2024.02.11

2024.02.10

2024.02.09

2024.02.07

2024.02.07

2024.02.06

2024.02.05

2024.02.02

2024.01.31

2024.01.30

2024.01.30

2024.01.29

2024.01.29

2024.01.27

2024.01.25

2024.01.24

2024.01.22

2024.01.16

2024.01.15

2024.01.14

2024.01.13

2024.01.12

2024.01.10

2024.01.04

2023.12.29

2023.12.29

2023.12.28

2023.12.27

2023.12.26

2023.12.25

2023.12.22

2023.12.22

2023.12.21

2023.12.20

2023.12.15

2023.12.15

2023.12.13

2023.12.12

2023.12.12

2023.12.11

2023.12.08

2023.12.08

2023.12.07

2023.12.07

2023.12.06

2023.12.05

2023.12.04

2023.12.04

2023.12.04

2023.12.03

2023.12.02

2023.11.30

2023.11.30

2023.11.29

2023.11.29

2023.11.28

2023.11.27

2023.11.25

2023.11.24

2023.11.24

2023.11.23

2023.11.23

2023.11.22

2023.11.21

2023.11.21

2023.11.17

2023.11.15

2023.11.14

2023.11.13

2023.11.12

2023.11.12

2023.11.11

2023.11.10

2023.11.10

2023.11.09

2023.11.08

2023.11.07

2023.11.06

2023.11.05

2023.11.03

2023.11.02

2023.10.30

2023.10.28

2023.10.28

2023.10.27

2023.10.26

2023.10.24

2023.10.20

2023.10.19

2023.10.18

2023.10.17

2023.10.16

2023.10.15

2023.10.12

2023.10.11

2023.10.10

2023.10.09

2023.10.08

2023.10.08

2023.10.06

2023.10.05

2023.10.04

2023.10.02

2023.09.30

2023.09.30

2023.09.28

2023.09.27

2023.09.26

2023.09.22

2023.09.21

2023.09.20

2023.09.15

2023.09.13

2023.09.11

2023.09.09

2023.09.08

2023.09.07

2023.09.07

2023.08.31

2023.08.30

2023.08.30

2023.08.29

2023.08.28

2023.08.21

2023.08.18

2023.08.17

2023.08.16

2023.08.15

2023.08.14

2023.08.09

2023.08.09

2023.08.08

2023.08.04

2023.08.04

2023.07.31

2023.07.28

2023.07.27

2023.07.24

2023.07.24

2023.07.23

2023.07.21

2023.07.20

2023.07.20

2023.07.19

.jpg?imageView2/1/w/400/h/300/format/webp)

2023.07.18

2023.07.17

2023.07.17

2023.07.14

2023.07.13

2023.07.11

2023.07.07

2023.07.06

2023.07.05

2023.06.30

2023.06.29

2023.06.28

2023.06.27

2023.06.26

2023.06.23

2023.06.22

2023.06.19

2023.06.17

2023.06.16

2023.06.15

2023.06.14

2023.06.14

2023.06.13

2023.06.13

2023.06.11

2023.06.09

2023.06.08

2023.06.08

2023.06.07

2023.06.07

2023.06.06

2023.06.05

2023.06.02

2023.05.31

2023.05.30

2023.05.30

2023.05.30

2023.05.30

2023.05.26

2023.05.25

2023.05.23

2023.05.21

2023.05.18

2023.05.17

2023.05.16

2023.05.15

2023.05.14

2023.05.11

2023.05.11

2023.05.09

2023.05.08

2023.05.06

2023.05.02

2023.04.28

2023.04.27

2023.04.27

2023.04.26

2023.04.24

2023.04.24

2023.04.20

2023.04.20

2023.04.19

2023.04.19

2023.04.17

2023.04.16

2023.04.13

2023.04.11

2023.04.11

.jpg?imageView2/1/w/400/h/300/format/webp)

2023.04.07

2023.04.07

.jpg?imageView2/1/w/400/h/300/format/webp)

2023.04.06

.jpg?imageView2/1/w/400/h/300/format/webp)

2023.04.05

2023.04.05

2023.04.03

2023.04.03

2023.04.01

2023.03.30

2023.03.30

2023.03.28

2023.03.28

2023.03.27

2023.03.24

2023.03.23

2023.03.22

2023.03.21

2023.03.21

2023.03.20

2023.03.20

2023.03.17

2023.03.14

2023.03.13

2023.03.13

2023.03.12

2023.03.10

2023.03.10

2023.03.09

2023.03.09

2023.03.05

2023.02.28

2023.02.27

2023.02.24

2023.02.24

2023.02.23

2023.02.21

2023.02.20

2023.02.19

2023.02.18

2023.02.18

2023.02.17

2023.02.16

2023.02.15

2023.02.15

2023.02.10

2023.02.02

2023.01.31

2023.01.23

2023.01.23

2023.01.22

2023.01.20

2023.01.19

2023.01.19

2023.01.18

2023.01.17

2023.01.17

2023.01.15

2023.01.12

2023.01.06

2023.01.06

2023.01.04

2022.12.26

2022.12.23

2022.12.20

2022.12.20

2022.12.18

2022.12.17

2022.12.17

2022.12.16

2022.12.15

2022.12.10

2022.12.10

2022.12.09

2022.12.08

2022.12.05

2022.12.04

2022.12.02

2022.12.01

2022.11.25

2022.11.25

2022.11.24

2022.11.23

2022.11.22

.jpg?imageView2/1/w/400/h/300/format/webp)

2022.11.22

2022.11.19

2022.11.18

2022.11.17

2022.11.15

2022.11.12

2022.11.11

2022.11.10

2022.11.10

2022.11.05

2022.11.03

2022.11.02

2022.11.01

2022.10.26

2022.10.25

2022.10.19

2022.10.19

.jpg?imageView2/1/w/400/h/300/format/webp)

2022.08.09

.jpg?imageView2/1/w/400/h/300/format/webp)

2022.08.07

2022.08.04

2022.08.04

2022.08.04

2022.08.04

2022.07.26

2022.07.22

2022.07.20

2022.07.15

2022.07.08

2022.07.07

2022.07.06

2022.06.24

2022.06.20

.jpg?imageView2/1/w/400/h/300/format/webp)

2019.05.07